Rejoice! Inflation Is Down and History Is Made as the Fed Stopped Trying to Kill the Economy!

Photo by Anna Moneymaker/Getty Images

Perhaps there is no subject with a wider gap between its immense importance and the sheer boredom it induces than monetary policy. It’s literally the price of money, but if I wrote a more sober headline of “Fed cuts 50 basis points and expects another 150 basis points of cuts by next year” then no one would click on this and I wouldn’t blame you. I know this because I already ran this experiment back at Paste Business in 2016 and I set all time internet records for least clicked articles every time I wrote about the Federal Reserve.

But then the hot inflation print of November 2021 changed the world, the Fed hiked interest rates at one of the fastest paces ever, the rent got too damn high, everything became more expensive, inflation rose to the level of front-page news, and I got a Master’s in Finance in between, so you really can’t get rid of my nerdiness now that it’s useful to help explain one of the most important issues facing Americans today.

Which brings us to today, a historic day in this new world with the highest interest rates in two decades.

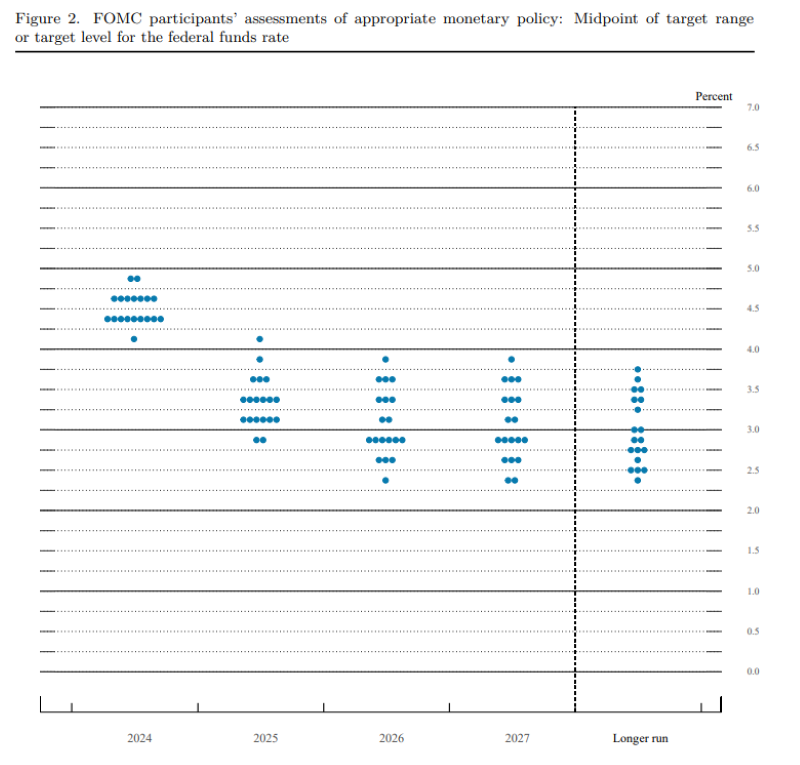

They’re coming down! And they will continue to come down until the Fed sees an uptick in inflation that worries them, or they hit their target where they plan to stop cutting. This means that borrowing costs for nearly everything will fall too. The basic dynamic behind monetary policy is that you lower interest rates to help borrowers and hurt savers to make people invest in the economy, and you raise them to do the opposite (which is why CEO of Ritholtz Wealth Josh Brown says that rich people actually love high interest rates because of the risk-free profit they get on their big piles of cash).

My title is hyperbolic, but it’s not an inaccurate description of the Fed’s goal since late 2021. The 1970s and 80s proved that if you raise interest rates, that will slow down the economy, and thus bring inflation down along with it. The Fed wanted to see the economy weaken, which it did, and the pain of high interest rates many have felt these past few years is a deliberate policy choice. They also wanted the labor market to cool off too, and Fed Chair Jerome Powell today said, “the labor market is not a source of elevated inflationary pressures,” so their war on workers seems to have ended as the Fed believes “inflation is…moving sustainably towards two percent.”

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-